Cheaper electricity - an emerging consensus?

It has been a busy 12 months - an opening apology for failing to update my substack!

I have spent much of the last year making the case for cheaper electricity in the UK. It feels like there is an emerging consensus here - aligning groups that are focussed on growth and those most concerned with decarbonisation. I think there are a few topics that have started to become areas of broad agreement.

I am trying to analyse energy in the UK to help improve policy. My writing reflects my personal views. None of the content should be construed as investment advice. I have done my best to ensure that the content below is accurate – but I am human and will make mistakes – if you spot any, please let me know and I shall update as appropriate.

1. Electricity is treated badly:

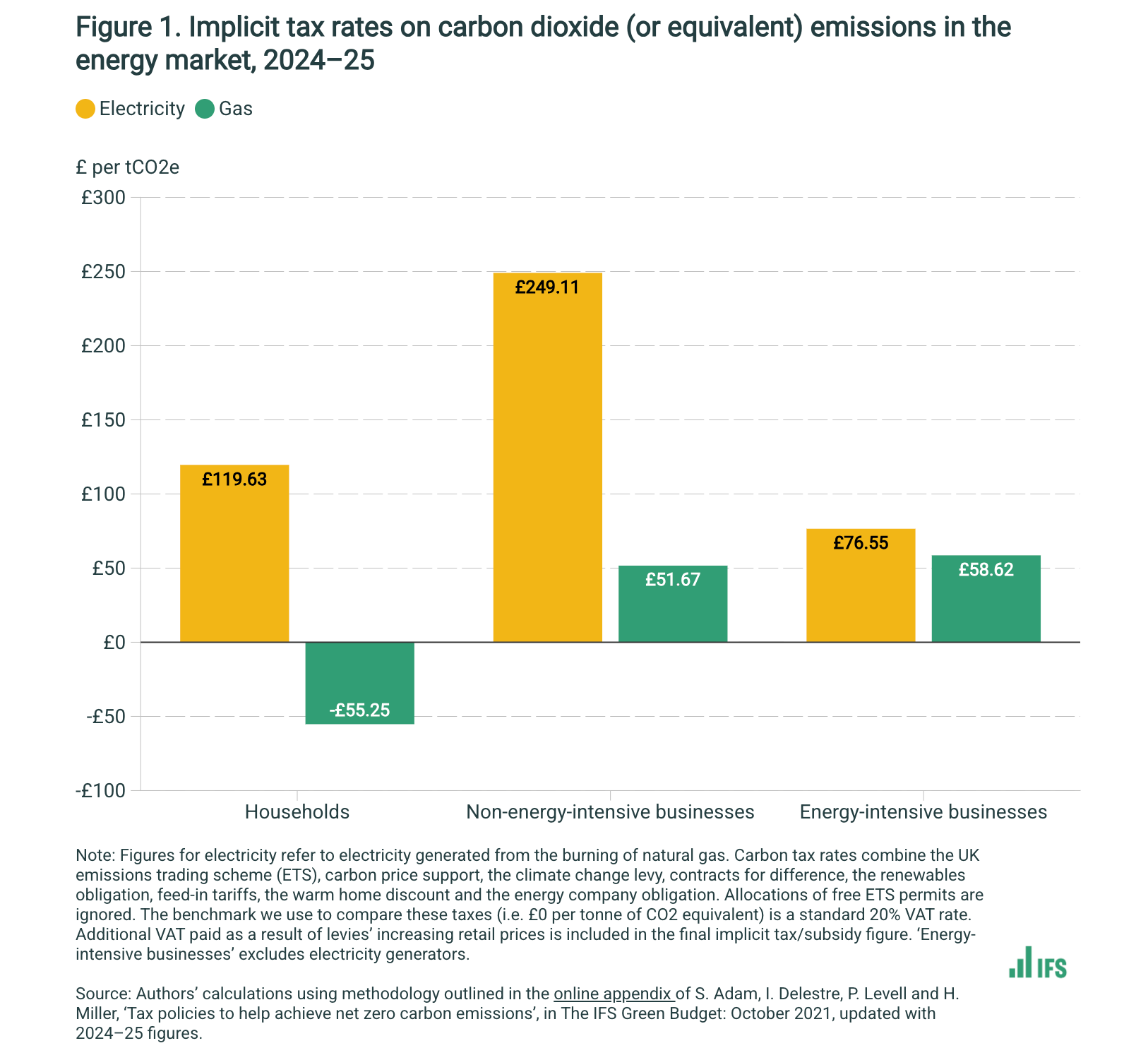

We have two carbon taxes on electricity - whereas domestic gas is largely untaxed. Electricity also suffers from legacy levies like the Renewable Obligation and the Feed-in-Tariff - both of which are major contractual burdens that act as a drag on electrification. This graph from the IFS sums up the picture quite nicely.

The electricity to gas price ratio will be around 3.6x based on the Ofgem price cap from July 2026. The ratio has improved a little thanks to higher gas prices and moving some electricity levies into taxation - but is still too high to make heat pumps compelling for most people.

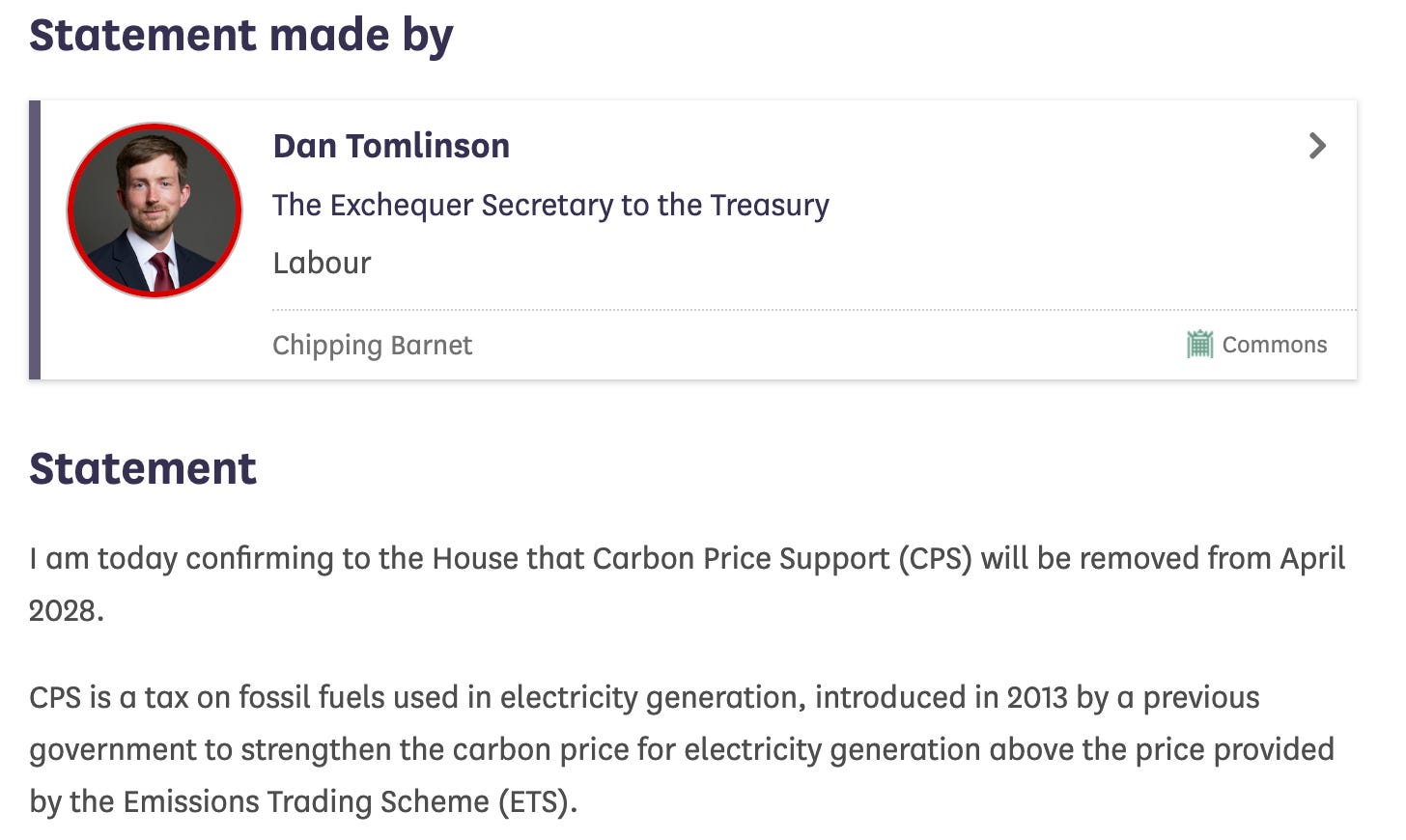

In October 2025 I made the case for removing the Carbon Price Support - a tax on gas power stations that increases wholesale electricity costs. I was thrilled to hear it will be removed from April 2028.

I would go much further on reducing electricity costs. I proposed a £4bn p.a. package that would reduce the domestic electricity to gas price ratio to around 3.1x in the short term, alongside more cost-conscious mechanisms for future procurement.

2. Stagnant electricity consumption is a problem:

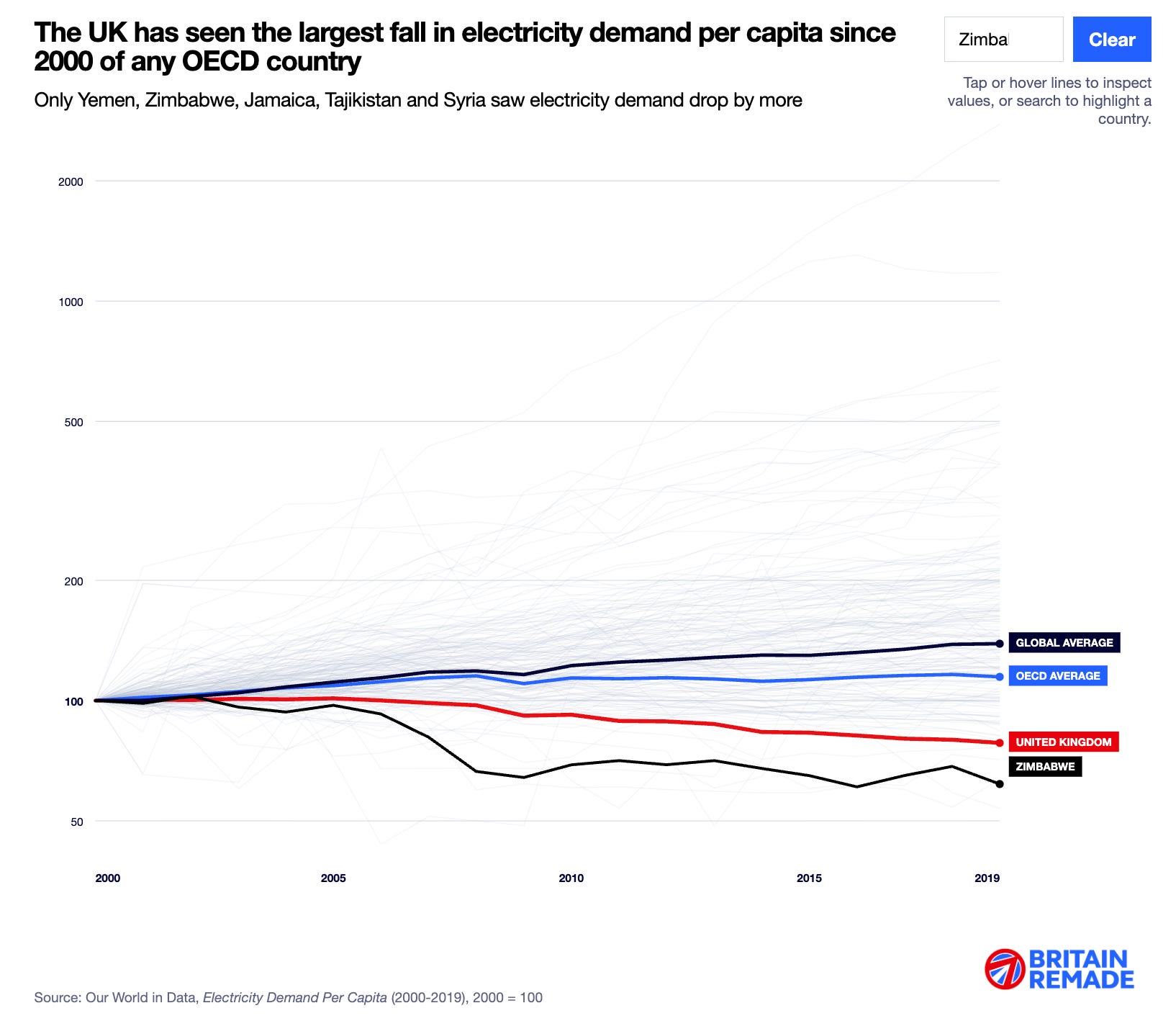

More organisations are recognising that the UK has an electricity consumption problem - we aren’t using enough of it. Britain Remade have noted that only Yemen, Zimbabwe, Jamaica, Tajikistan and Syria have had a faster decline in electricity consumption per capita since the millennium.

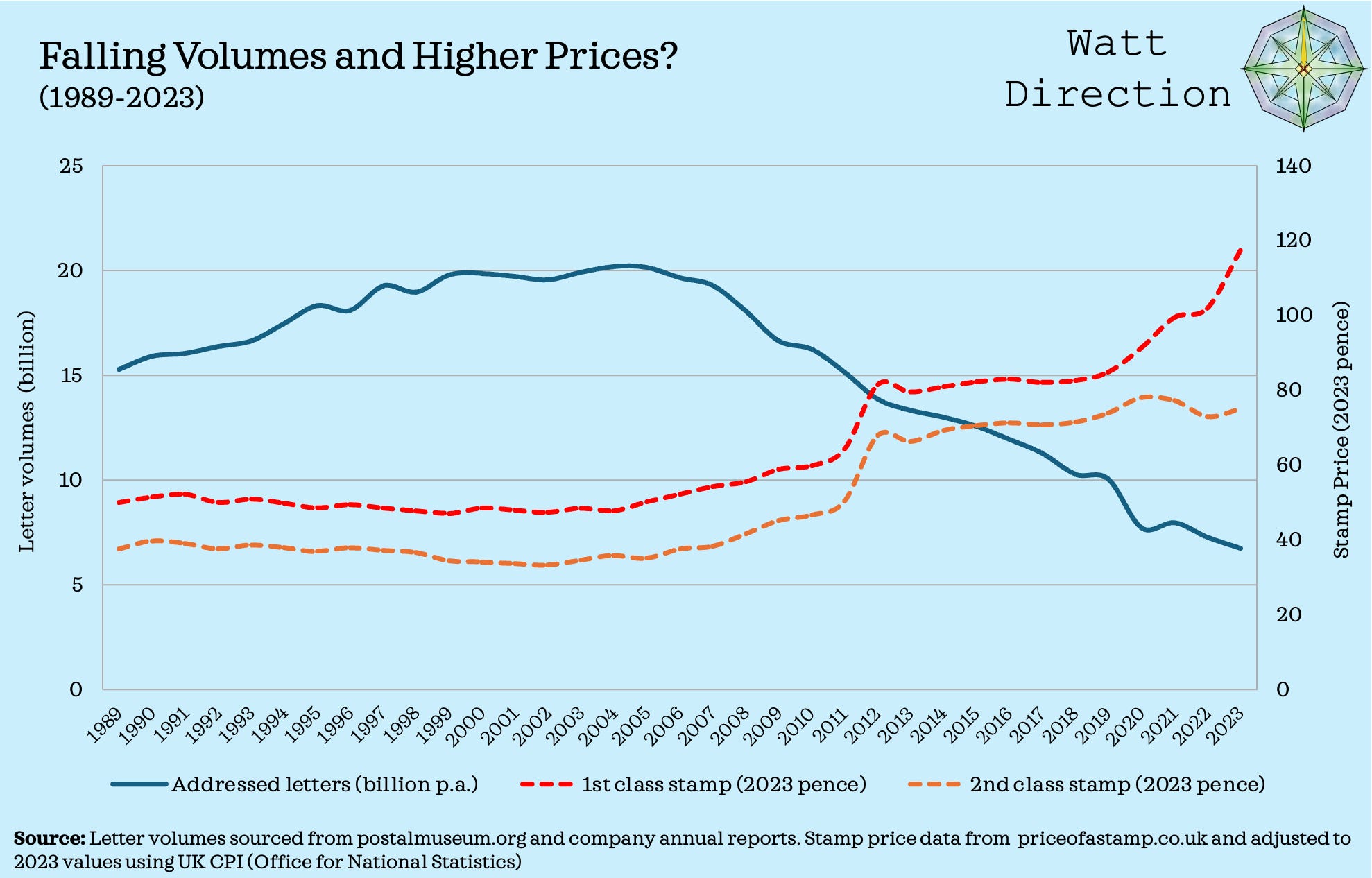

I am a relative newcomer to energy policy, with around two years of dedicated focus on the topic. Being an ‘outsider’ can be helpful - in my prior career as an equity analyst, I looked at hundreds of different businesses. Every business and industry is unique - but there are patterns. One of the patterns I learnt over time was to avoid businesses with a high fixed cost base and declining volumes.

The graph below is from UK postage industry. Once letter volumes went into decline, stamp prices had to increase to keep the system functioning. Higher stamp prices meant further volume declines, creating a vicious cycle.

The UK electricity system is in a bad place - because fixed costs are increasing dramatically and power is already expensive. Networks are being expanded and will need to be paid for. Variable costs are declining as we move away from fuel-based generation and towards capital heavy renewables and nuclear.

Meanwhile the importance of price as a driver of volume growth appears to be an afterthought! The National Energy System Operator (NESO) assumes that electricity consumption will rise by 11% by 2030 as part of their Clean Power 2030 analysis. But price isn’t a driver in this forecast - the volume growth assumption is driven by climate targets, not economic rationality or any analysis of price elasticity.

It is shocking how little attention has been paid to electricity costs. My proposals to scrap carbon taxes on electricity and move some of the levies into general taxation will attract criticism - but there aren’t a plethora of good options here.

My fear is that policy makers have been acting with a logically incoherent set of assumptions - adopting the ostrich strategy of burying heads in the sand and hoping it would all be fine as fixed costs piled up.

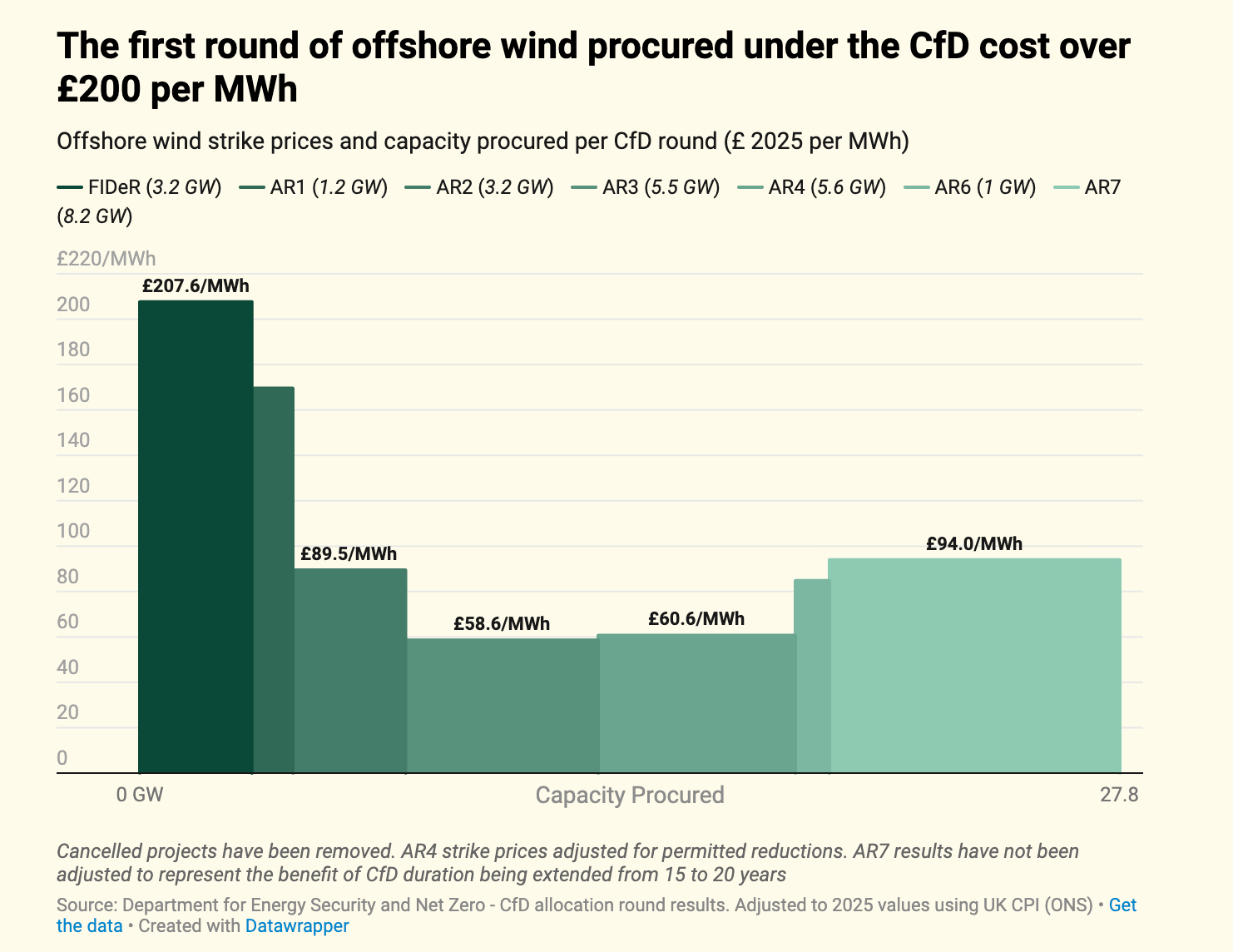

3. Offshore wind is getting more expensive:

Offshore wind was the first area of investigation on my substack. It quickly became apparent that assumptions from DESNZ and the Climate Change Committee didn’t resemble the empirical evidence I had collected from company accounts.

The graph below shows that there has been a big cost inflection since the projects of AR4 and AR5 (c. £60/MWh) were announced in 2022 and 2023 respectively.

The good news is that DESNZ have updated their own cost assumptions. For example, their 2023 cost assumptions assumed a 69% load factor for an offshore wind project commissioning in 2035. The equivalent document from 2025 had cut that back to a much more sensible 49%.

It is good that DESNZ have updated their numbers. My worry is that this hasn’t been noted more widely - with many preferring to adopt the ostrich strategy and pretend that £94+/MWh for intermittent generation is somehow a bargain.

By contrast, solar and onshore wind cleared at £68/MWh and £75/MWh in 2025 prices in AR7.

Wind and solar have their place on the electricity system - but in my view they are only valuable to the extent that they save fuel and carbon, as they provide minimal firm capacity. In a gas heavy system, the fuel and carbon saving can be material and justify their presence. If the UK ever sorted out its nuclear construction costs and built out a massive fleet, the fuel and carbon savings would be minimal and much lower wind and solar capacity would be justified.

4. Transmission spending needs attention:

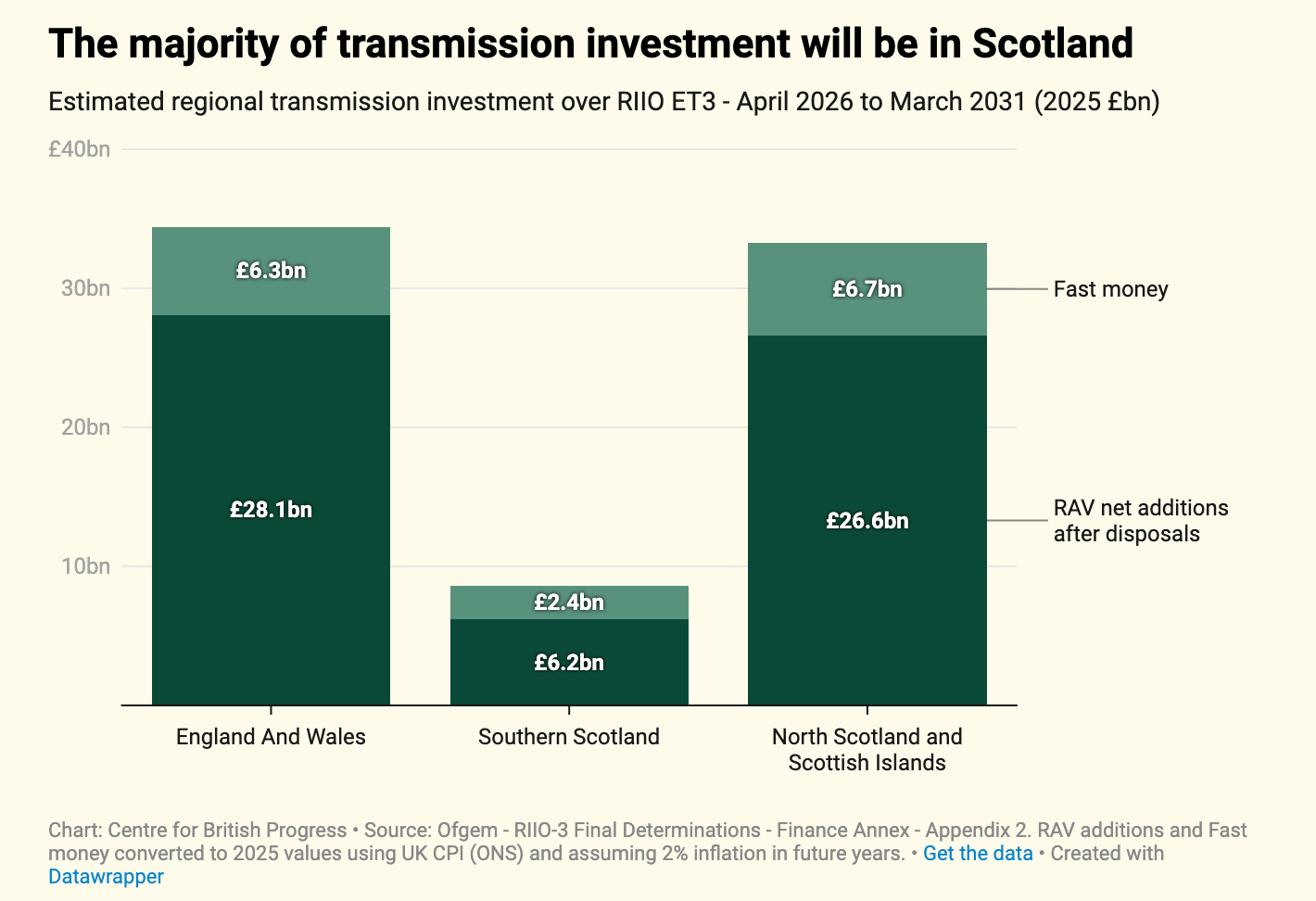

The new control period for electricity transmission spending has started, with over £70bn of network upgrades expected over the next five years. £70bn is a serious chunk of change - and the investment will be recovered through consumer bills, much of it over a 45 year depreciation period.

This source of bill cost inflation is starting to focus minds - The electricitybills.uk website assumes that household transmission costs will roughly double between 2025 and 2030, from £52 p.a. to around £105 p.a.

Some transmission upgrade work undoubtedly needs to happen - but this area is starting to attract attention due to the massive levels of investment and future bill pressure. I think there are good options for saving money here - zonal or nodal pricing would help expose generators to grid limitations in their area, incentivising them to locate in places more beneficial to the system.

Policy makers have an unwelcome tendency to shy away from attributing a lot of the grid upgrade costs to wind generation. A very simple test for me is looking at where the spending is expected to occur - there is a very significant skew towards Northern Scotland - to increase boundary transfer capacity and make better use of onshore and offshore wind.

I’m often told this level of expenditure is due to ‘historic underinvestment’ or has ‘nothing to do with renewables’. I would politely point out that our electricity networks of 20 years ago delivered around 27% more power than they did in 2024. We have moved to a much lower utilisation system that requires much more grid investment for each unit of delivered power.1

5. System costs need to be understood:

Part of the reason that the UK energy debate has become fractious is because different parties are making arguments using very different sets of notes.

Those in favour of very high levels of intermittent renewable capacity will talk about low marginal costs, ignoring the fact that renewable generators receive substantial compensation outside of the wholesale market.

‘Levelised costs’ (which account for average generation costs over the life of a project) become something of a middle ground, but still ignore the costs of intermittency, treating a MWh of power as fungible through time and space.

System costs account for the total cost of the power system and are the most useful lens to look at the electricity system. But they are more difficult to calculate - and might generate unwelcome conclusions for the current Energy Secretary!

We need better analysis from our public institutions - DESNZ, Ofgem and NESO. It is shocking that the best analysis of household electricity costs over the next 5 years come from a private website rather then one of these much better resourced organisations.

These entities have a lot of very talented people working for them and can clearly do the work - we have good evidence that the intellectual horsepower exists:

DESNZ (then BEIS) modelled ‘enhanced levelised costs’ (that accounted for networks, balancing, the capacity market and ancillary services) back in 2020

Ofgem are reviewing how system costs are allocated and recovered

NESO analysed the Clean Power 2030 plan at a system cost level

My long term preference would be to move away from central planning, and instead design a market where generators internalise the wider costs they impose on the electricity system.

6. Trade-offs are real:

The UK energy debate has moved away from energy ‘cakeism’ and is starting to engage with very real trade-offs.

The carbon intensity of our electricity generation system is a good example. Adding the first few percentage points of intermittent generation to the system didn’t impose much in the way of extra costs - the UK had spare network capacity thanks to falling consumption volumes. It could also shut down old coal power stations and run its gas plants at slightly lower utilisation.

But this gets more difficult as the proportion of intermittent generation increases - networks, interconnectors, storage, demand side response and voltage/frequency services all need to be added to the system.

There is a reason that Clean Power 2030 adopted a 95% definition for clean power, with unabated gas making up 5% of generation. To summarise page 53 of NESO’s Clean power 2030:

“Once a clean power system is reached by 2030, further reducing the share of unabated gas below 5% by building more clean power capacity becomes very difficult.”

Doubling battery power & capacity reduces gas use by sub 0.1 percentage points

More interconnection won’t reduce gas use any further

Adding more wind and solar “has a very limited impact on unabated gas use”

If 1.8 GW of nuclear was added, around 25% of its generation would displace gas, with the balance curtailed or exported at low prices.

Moving beyond 95% runs into rapidly diminishing returns. But a very similar logic should apply to 90%, 85% or 80% clean power if the envisaged system is designed around renewables plus gas backup.

Page 31 of the Clean Power 2030 report has an interesting line - if we didn’t spend tens of billions expanding the grid, we would be capped at 91.9% clean power not 95%.

I’m not making a judgement on the grid build out either way - but there is a trade-off here. I suspect most consumers might prefer £50 lower electricity bills in exchange for a marginally higher role for gas!

It might even be the best strategy from a decarbonisation perspective - 5% lower household electricity prices would encourage the electrification of heating and transport.

7. Energy security remains high on the agenda:

Events in the Middle East have led to another spike in fossil fuel prices - though the bigger price spikes have been in oil and refined products rather than natural gas.

I was hoping that this would lead to a more rational debate on the North Sea - i.e. allowing new licenses. The phrasing in the Labour Party Manifesto 2024 is interesting - banning new licenses on the grounds of bill impact, energy security and climate concerns.

“We will not issue new licences to explore new fields because they will not take a penny off bills, cannot make us energy secure, and will only accelerate the worsening climate crisis.”

But new licenses would create longer term tax revenues, improve physical energy security, and reduce the emissions intensity of UK gas supply. So, I think this stance is incorrect on all three counts!

Energy security means different things to different people. Aside from physical security of energy supplies, I think price stability is an interesting topic.

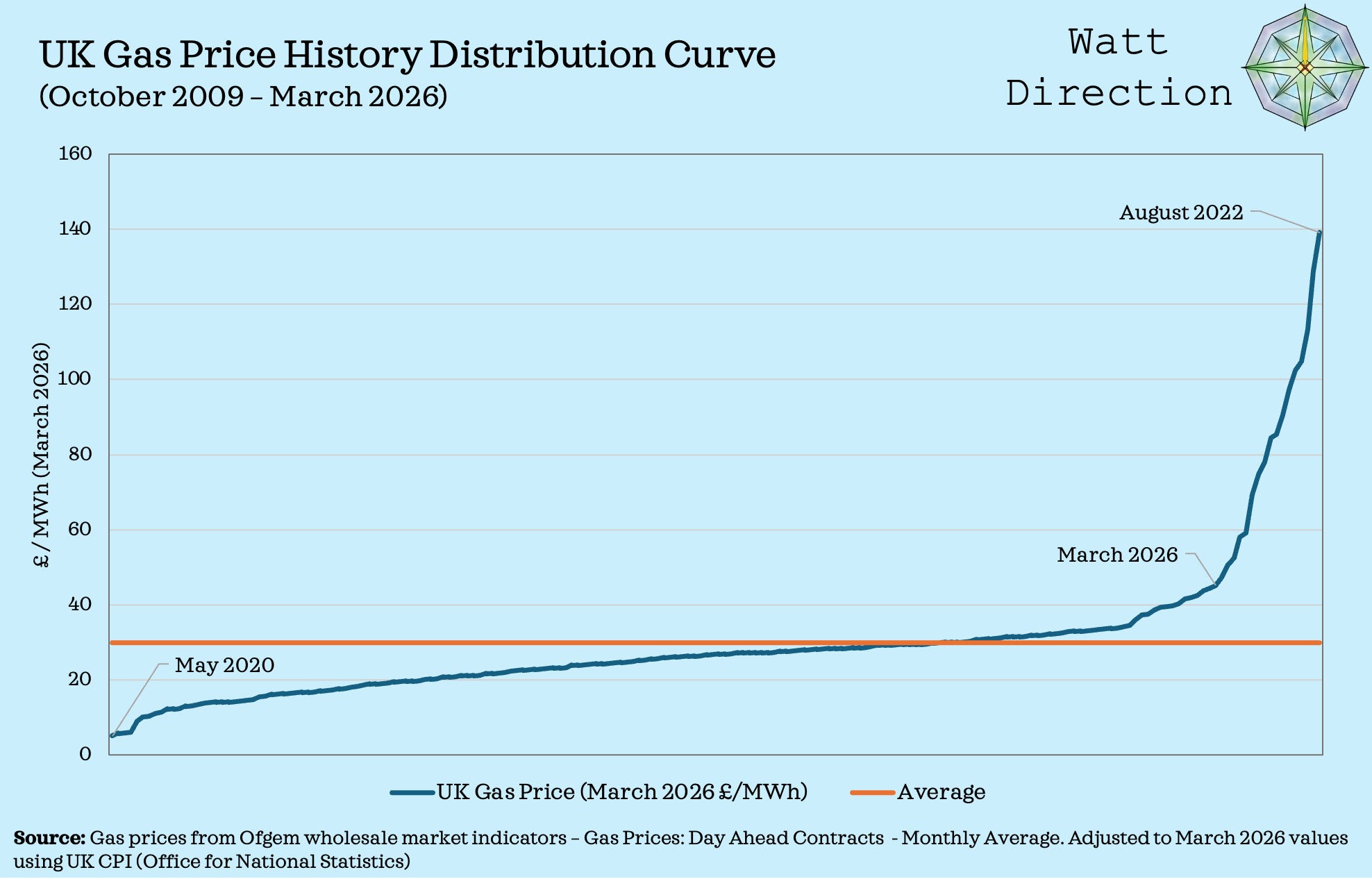

The graph below plots monthly UK gas prices since October 2009 in an ascending curve. The prices have all been adjusted to March 2026 values. The price history shows substantial ‘right tail’ skew - nearly 70% of months were below the average, which is buoyed up by very extreme gas prices in 2022.

Part of the long term consumer proposition for electrification could be greater price predictability and stability. Behavioural economics would suggest humans are loss averse - feeling the pain of negative shocks much more acutely than an equivalently sized financial gain.

A strong preference for avoiding large negative shocks is rational - I buy insurance to protect against large negative financial shocks that would materially impact my life.

The impact of gas prices on the retail price of electricity is set to weaken over time - gas is already setting the wholesale price less often, and more of our generation costs will be secured away from spot markets - via CFDs and the Regulated Asset Base model.

My concern is that that this argument can be taken too far - and risks locking in prices that might look ok for now but are less attractive if gas prices fall.

For example, I am critical of the “Wholesale Contract for Difference” proposal that will allow generators already supported by the Renewable Obligation to fix the wholesale part of their income. I don’t want to subsidise generators twice, and I’m worried that applying CFDs to more and more of the market will have adverse consequences.

Closing Thoughts:

UK energy policy could learn a lot from Adam Smith. We need to build an electricity system that works for consumers, rather than serving the interests of producers.

“Consumption is the sole end and purpose of all production; and the interest of the producer ought to be attended to, only so far as it may be necessary for promoting that of the consumer”

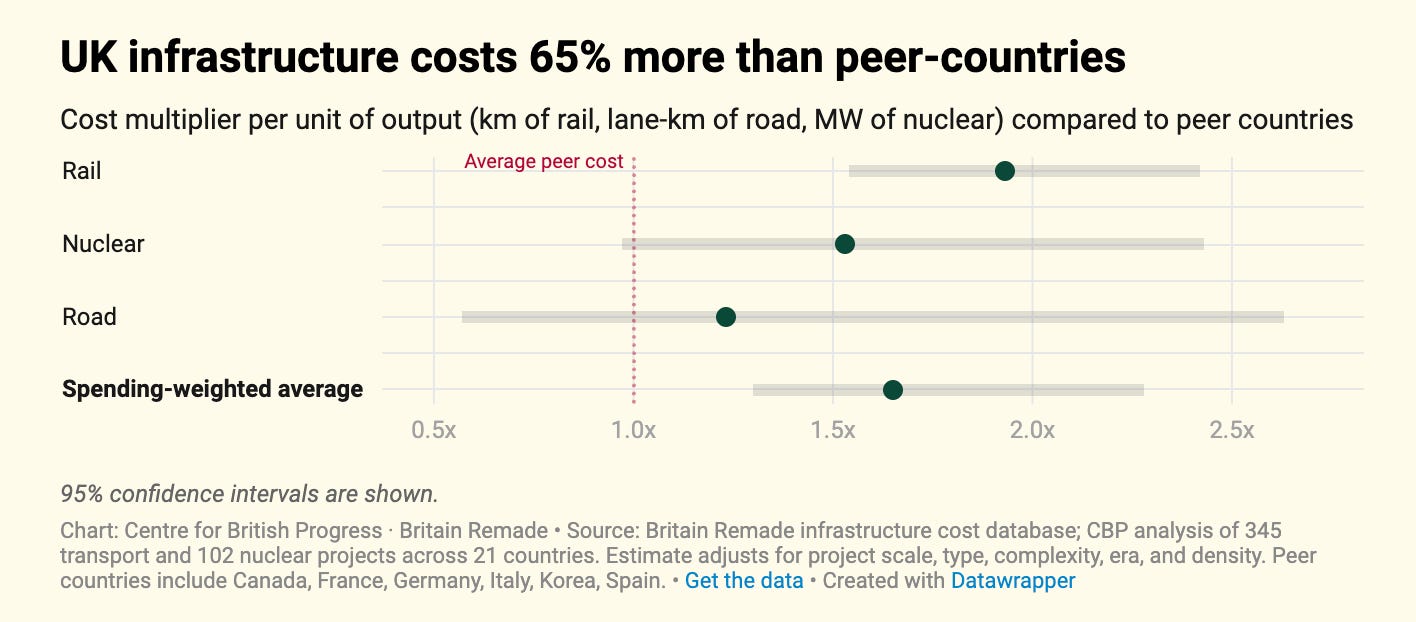

It may also be the case that I am guilty of fighting over a narrow local optimum. A recent paper from the Centre for British Progress highlights that infrastructure projects are costing much more to deliver in the UK than in peer countries. Building transmission, nuclear and renewables at lower costs would be a more powerful long term lever than mix optimisation!

On a personal note, I am about to start a new role at Onward, leading their energy research. Please get in touch if you have policy ideas that could help lower costs, improve energy security or drive cost effective decarbonisation!

I have enjoyed an amazing twelve months at the Centre for British Progress and it is a wrench to leave - the team are brilliant and have taught me so much. Please do check out their research - my former colleagues have written amazing papers on tax cliffs, the pension triple lock and stamp duty reform.

It is easy to be negative on the UK with our stagnant economy and political drama - but I feel much more positive knowing that there are brilliant people working very hard to try and improve things.

Thanks for reading!

DUKES table 5.1 - electricity commodity balance (GWh). Statistic compares electricity final consumption in 2006 vs 2024 levels.

Dear Mr Hezlet, Thank you for your piece from which I learned several things.

But in judging the worthwhileness of our transitioning to renewables I thought you missed two important points.

1) Its not only about climate. Installing rooftop solar is like a second mortgage - this one saves you paying for energy bills life long.

2) Transitioning to renewables saves the UK import bill on the imported fossil fuels. So our balance of payments will be less in the red, a good aim I would think.

3) For the UK to transition helps put pressure on oil exporters to look at other alternatives - eg exporting electricity instead.

4) Electric road vehicles have same effect, so another reason to embrace these as well.

5) What are the costs of transitioning our railways to all electric, I wonder? Again would reduce our imports of oil still further.

Well a few thoughts for you. be interested in your answers. Ian

Ed … from my perspective it’s been a year well spent.

Excellent article, useful insights and some refreshingly pragmatic suggestions (that’s a compliment by the way from a jaded engineer who has read far too many ‘thoughts’ on energy policy from policy wonks) for how to move forward.

Good luck with the new gig.